One of the number one topics we’re asked about is where to invest money. I, Johnny, am excited to tackle this question in this edition of our Money Talks Finance Series. It literally feels like everyone is in the game and winning (please normalize sharing your losses, too, folks).

Lots of talking heads say the market is frothy (and it is), but they also pounded into our heads for a decade when the market pulls back -20%, it’s a generational buying opportunity. If you missed the wave that was 2020, you probably feel like you missed the boat. Don’t worry, you didn’t. I think the number one reason people lose when it comes to investing, is simply not investing at all. You can’t win the game if you’re on the sidelines.

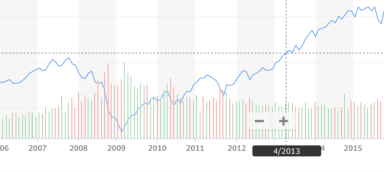

Let’s take a quick look back for anyone who began investing shortly after the 2008 Great Financial Crisis. 367% gain. This is something you can only appreciate in hindsight, but something you can only benefit from if you put your money to work.

It’s not all rosy 100%+ gains. Prior to the crisis, the S&P 500 peaked and didn’t return to the peak for 5+ years. It dropped roughly 50% from peak to trough. Absolutely gut-wrenching stuff.

2020 and 2021 definitely minted a lot of the newest traders and “investors” than I’ve ever seen. Active investing is hot again! I had my own new experience trading options for the first time in 2020. We’ve even had friends contemplate starting hedge funds.

The general principle of investing is you’re giving up consuming today for consumption tomorrow. I joke all the time “future Johnny” will hopefully thank “past Johnny” for making a good decision and turning a $1 today into hopefully $10.

So, you want to know how and where to invest money? Let me introduce you to our capital stack.

WE ARE NOT FINANCIAL ADVISORS. THE CONTENT IN THIS POST IS FOR EDUCATIONAL PURPOSES ONLY AND MERELY CITES OUR OWN PERSONAL OPINIONS. IN ORDER TO MAKE THE BEST FINANCIAL DECISION SUITING YOUR OWN NEEDS, YOU MUST CONDUCT YOUR OWN RESEARCH AND SEEK THE ADVICE OF A LICENSED FINANCIAL ADVISOR IF NECESSARY. KNOW ALL INVESTMENTS INVOLVE SOME FORM OF RISK AND THERE IS NO GUARANTEE THAT YOU WILL BE SUCCESSFUL IN MAKING, SAVING, OR INVESTING MONEY; NOR IS THERE ANY GUARANTEE THAT YOU WON’T EXPERIENCE ANY LOSS WHEN INVESTING. ALWAYS REMEMBER TO MAKE SMART DECISIONS AND DO YOUR OWN RESEARCH!

Spending/Banking

Chase Banking + Chase Sapphire: For all the grief major banks seem to get, I’ve actually had a relatively great time banking at Chase. When I started out, I was a Washington Mutual customer before 2008 when they went out of business and got swallowed up by our friend Jamie Dimon (CEO of Chase). Since then, The Points Guy and Chase came together and created the best general-purpose credit card in the game for points/rewards folks. This is mainly what we used to get to South Korea for the Winter Olympics and Hoang-Kim recently cashed in some points to fly her Mom first class to New York.

Customer service has always been elite and we’ve basically used points to do any international travel. For the BNPL (buy now, pay later) folks, Chase actually has “My Chase Plan” that allows you to break up large charges on your card into even smaller, more manageable ones (ex. $1000 > 6, $166 monthly payments).

Roboadvisor

Betterment – This is what we think of immediately when people ask where to invest money. It’s what we use today and it’s stupid-proof, which is great for me. You deposit your money, set your risk tolerance, any goals and it’ll invest for you accordingly. It’s the first place I recommend to people who are just getting started investing and want to do it in a smart and risk-adjusted way. This is your solution for access to stocks and bonds. The average return expectation is ~7% per year. We also have a high-yield saving account with Betterment and you can easily deposit and withdraw money anytime you like without any fees. Hoang-Kim just took some money out of her wedding account on Betterment and was hit with $12 in taxes because of her gains. I find it helpful they automatically calculate and manage all reporting as well.

Before we continue on where to invest money, let’s remember great investing is soooo boring. Sometimes worse than watching paint dry because compounding takes so long to see. For context, Warren Buffett made 99.7% of his wealth after he was 52. Most people would be best served getting and staying out of debt, setting up and investing in tax-advantaged accounts, then depositing capital into Betterment. For most people, that’s where it ends. Go enjoy your life.

If you’re interested in getting exotic, keep reading.

Real Estate

Fundrise – Typically people invest in REITs (real estate investment trusts) to access institutional real estate portfolios. The average return expectation is 8-15%+.

I looked at investing into real estate through talented friends since college, but typically minimums were $25k to buy into one apartment complex. I discovered Fundrise as one of the first general access private real estate funds that had very low minimums and allowed me to invest into multifamily real estate across the US, so I invested in their Growth eREIT when it opened up years ago and have seen ~14% annual growth. This is not a liquid investment, so I’ve only been able to receive cash dividends but otherwise will sell when the fund concludes its life in another 5+ yrs. This was very much an example of investing $1 so I can spend $2+ in 10 yrs.

Brokerage

- Robinhood (RH) – I’m not a high-brow investor with super-sophisticated tools. Like you, if I want to buy just one share of a business you like, cost matters a lot. I personally like to keep costs low when when considering where to invest money. Fees are an enemy of long term gains. Commission-free trading is great and it’s hard for me to take haters on it seriously. My first lesson as a kid was trading on Schwab back when trades were $7.95 and I started with $1000. I ended up losing $500 to commissions. Stupid mistake as a kid that was worth learning. Luckily I also forgot the password and left it alone and my first buys were AAPL and TSLA. Goes to show if you place your bets correctly and leave well enough alone, you’ll do just fine.

- Some would say it’s unhealthy, but RH made options trading stupidly easy. Before RH, I didn’t really quite understand how options worked and how to make money with them. I usually just heard stories of how people blew themselves up. When considering where to invest money, it’s worth learning about options trading if you’ve got the stomach and attention span for it to generate some outsized returns.

- Personally, I stick with what people call LEAPS. While some people invest in short-term options, I like to invest in options that expire in 12+ months. I’m generally bad at guessing both velocity, which is direction (up or down) and speed (by when). LEAPS allow me to magnify my bets on companies I believe in longer-term with some leverage. It’s one of the few tools for me personally where I can invest $1k with the possibility of turning it into 5-10k, but only risk listing 1k. Coming from venture capital, I’m constantly looking for asymmetric bets (lose 1x, but gain 10x).

- Schwab – I’m not actively on Schwab, but our financial advisor is a big fan as someone who came from a family office (dedicated investing office for people with way more commas in wealth than us). He’s managing our accounts using institutional tools the wealthy have access to. Schwab gives nearly universal access to every fund imaginable to custom tailor your portfolio to your needs. Oh and something he told me about I didn’t quite understand before is Schwab allows you to lend against your account value. Given interest rates today, this isn’t the worst option if you have some capital expense you need to make without selling your positions. I’ve heard Robinhood say they do this, but haven’t seen it.

Crypto

- Coinbase – For the longest time, I didn’t like Coinbase because the fees it’d charge me for each purchase of crypto when Robinhood would allow me to buy crypto commission-free. What makes the fee worth it on Coinbase is the access to multiple other tokens beyond BTC, ETH, and DOGE. Ex. I’m a fan of Uniswap, Numeraire, and Storj. On Robinhood, I don’t have access to these. Even more importantly I can’t transfer my BTC or ETH to any other wallets on Robinhood. If you want to move it off Robinhood, you need to liquidate it. Most importantly, Coinbase is more secure, works closely with regulators, and actually has customer service unlike many of the wallets and exchanges. For what it’s worth they’re also a public company ($COIN)

- Metamask – This one is for people who want to get deep into crypto. Metamask is an ethereum (ETH) wallet letting you interact with decentralized applications. All the traders who want to begin doing more advanced things like “yield farming” or onboard into more advanced trading platforms like FTX (yes the sponsor of the Miami Heat Stadium)

What’s Next?

For me, when someone asks where to invest money, it usually is code for “tell me what stock to invest in so we can get rich together.” If you’ll indulge me, I’d really love it if you replied with your investing situation and thoughts or a company you’re either interested in investing in or have invested in. I love discussing this stuff all day and learning about what people are seeing and their conviction (size of bet) in their observations.

If you do one thing after reading this, GET INVESTED. Time is the one advantage you have that is constantly depreciating. We gifted a friend’s one year old daughter $50 to invest in her future. Why? Because she’s a time multibillionaire if you’re counting in seconds. We want her to use it wisely!

Nordstrom Anniversary Sale 2021 Preview Picks

TOPS & SWEATERS

BOTTOMS

BLAZERS & COATS

ACTIVE

ACCESSORIES & SHOES

BEAUTY